Mobile Home Titles: Personal Property vs Real Property (and Why It Matters)

By Uncle Zally · May 2026 · 6 min read

Most people shopping for a mobile home dont think twice about the title. They figure its like buying a car — sign the papers, get the keys, done. And honestly, thats not completely wrong. But heres the thing: how your mobile home is titled changes almost everything about what you can do with it later. Your financing options, your taxes, even what happens to it when you pass away — all of that traces back to one question.

Is your mobile home personal property, or real property?

What “Personal Property” Actually Means for a Mobile Home

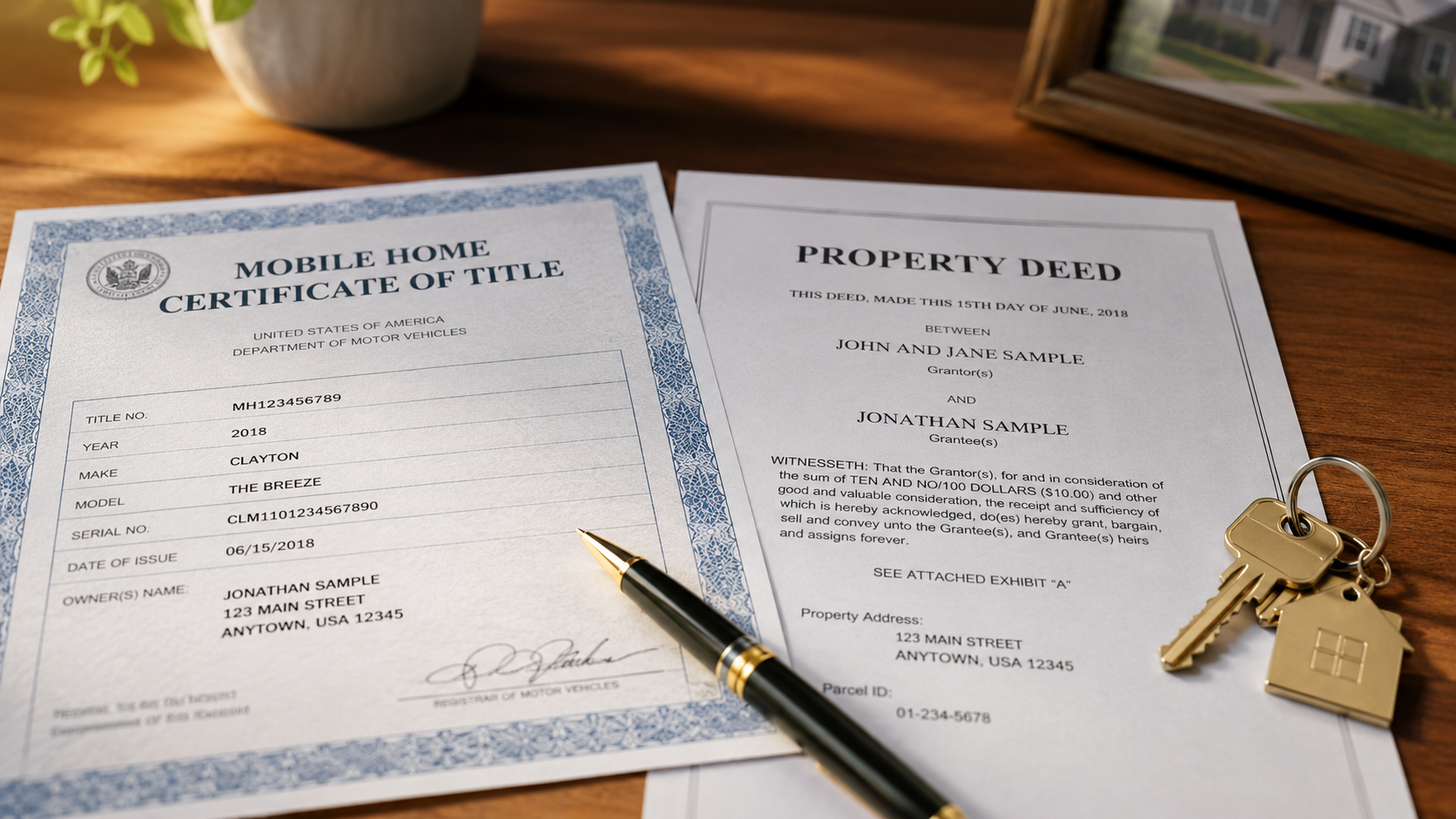

When a manufactured home rolls off the factory floor, it gets a certificate of origin from the manufacturer. Think of it like a birth certificate for the home. From that point on, the home is legally classified as personal property — the same category as your car, your boat, or your riding mower. About 75% of all manufactured homes in the U.S. still carry this classification right now.

As personal property, your mobile home gets titled through your state’s DMV or motor vehicle division. Yeah, the same place you register your truck. The title looks similar too — its a certificate of title, not a deed. You pay personal property taxes on it instead of real estate taxes, and in most states those are lower. Sounds like a win, right?

Not exactly. Being classified as personal property comes with some real downsides that catch people off guard.

For starters, most traditional mortgage lenders wont touch a personal property mobile home. You’re stuck with what’s called a chattel loan, which is basically a personal property loan. These carry higher interest rates — sometimes 2 to 4 percentage points above a regular mortgage. On a $60,000 home, that difference can cost you $15,000 or more over the life of the loan. Thats real money.

Personal property mobile homes also tend to depreciate rather than appreciate. Just like a car loses value the second you drive it off the lot, a mobile home classified as personal property often loses value over time. Not always — location matters a lot — but the trend works against you.

When Does a Mobile Home Become Real Property?

Here’s where it gets interesting. A mobile home can be converted from personal property to real property, and doing that opens up a whole different world of options. But you cant just declare it real property because you feel like it. There are actual requirements.

The basic rules in most states boil down to three things:

First, you have to own the land underneath the home. If you’re renting a lot in a mobile home park, your home stays personal property no matter what. The home and the land need to be under the same ownership.

Second, the home needs to be permanently attached to the land. That means a real foundation — not just sitting on blocks or a temporary setup. Most states require the wheels, axles, and tongue (the hitch) to be removed. The home needs to be anchored to a permanent foundation that meets local building codes.

Third, you need to go through the legal process of retiring the vehicle title and recording the home as part of the real estate. This is the paperwork part, and it varies by state — but it usually involves filing an affidavit of affixture with your county recorder and surrendering the old certificate of title to the DMV.

Why Would You Bother Converting?

Fair question. The conversion process isnt free, and its not instant. Depending on your state and whether you need foundation work, you could spend anywhere from a few hundred dollars on paperwork alone up to $8,000 or more if you need a new foundation poured. So why do it?

The biggest reason is financing. Once your mobile home is real property, you qualify for conventional mortgages, FHA loans, VA loans, and USDA loans. These programs offer interest rates that are typically 2 to 4 points lower than chattel loans. Over a 20 or 30 year loan, the savings from that lower rate will usually dwarf what you spent on the conversion.

Real property mobile homes also tend to hold their value better. Some even appreciate, especially if they’re on owned land in a good area. When its time to sell, buyers can get regular mortgages to purchase your home, which means a bigger pool of potential buyers and usually a higher sale price.

There’s a tax angle too. Real property owners can deduct mortgage interest on their federal taxes. Personal property loan interest? Not deductible. If you itemize your deductions, that’s another chunk of savings.

The Conversion Process (State by State, It Varies)

I wish I could give you one simple checklist, but every state handles this differently. Some states make it pretty straightforward. Others make you jump through hoops. Here’s the general process though.

You’ll start by getting the home permanently set on a foundation that meets your state and county requirements. If its already on a permanent foundation, you’re ahead of the game. If not, you’ll need a contractor — foundation costs for a single wide typically run $4,000 to $12,000 depending on the soil conditions and your area.

Next, you’ll need to file paperwork with your county. In most states this includes an affidavit of affixture, which is a legal document stating the home is permanently attached to the land. Some states also require a surveyor to confirm the home’s location on the property.

Then you surrender the certificate of title (the DMV title) to your state’s motor vehicle agency. They’ll cancel it. From that point forward, the home is described in your property deed just like a stick built house would be.

The whole process takes anywhere from 30 days to several months depending on your state. Florida, Texas, and North Carolina all have slightly different procedures, and some counties within the same state move faster than others. Check with your county recorder’s office — they deal with these conversions regularly and can tell you exactly what’s needed locally.

One Big Warning About Title Issues

If you’re buying a used mobile home, check the title carefully before you hand over any money. Title problems with manufactured homes are more common than you’d think. The previous owner might not have the title at all. Or the home might have a lien on it from an old loan that was never properly released. In some cases, the home was moved from another state and the title was never transferred correctly.

A missing or messy title can delay your purchase by weeks or months, and in worst case scenarios it can kill the deal entirely. Always verify that the seller has a clean title in their name before you sign anything. Your states DMV can usually do a title search for a small fee.

Uncle Zally Covers This Stuff and More

Titles, deeds, financing, inspections — theres a lot to keep track of when you’re buying a mobile home. Uncle Zally breaks all of it down in plain English in his book. Its $19.95 and comes with three bonus guides that cover everything from negotiating with dealers to picking the right park. Grab a copy here before you sign anything.

Ready to Buy Smart?

Uncle Zally’s book walks you through every step of financing, negotiating, and closing the deal on a mobile home. Plus you get two bonus books free.